UK-Iceland power cable needs 1,459 MW of new capacity

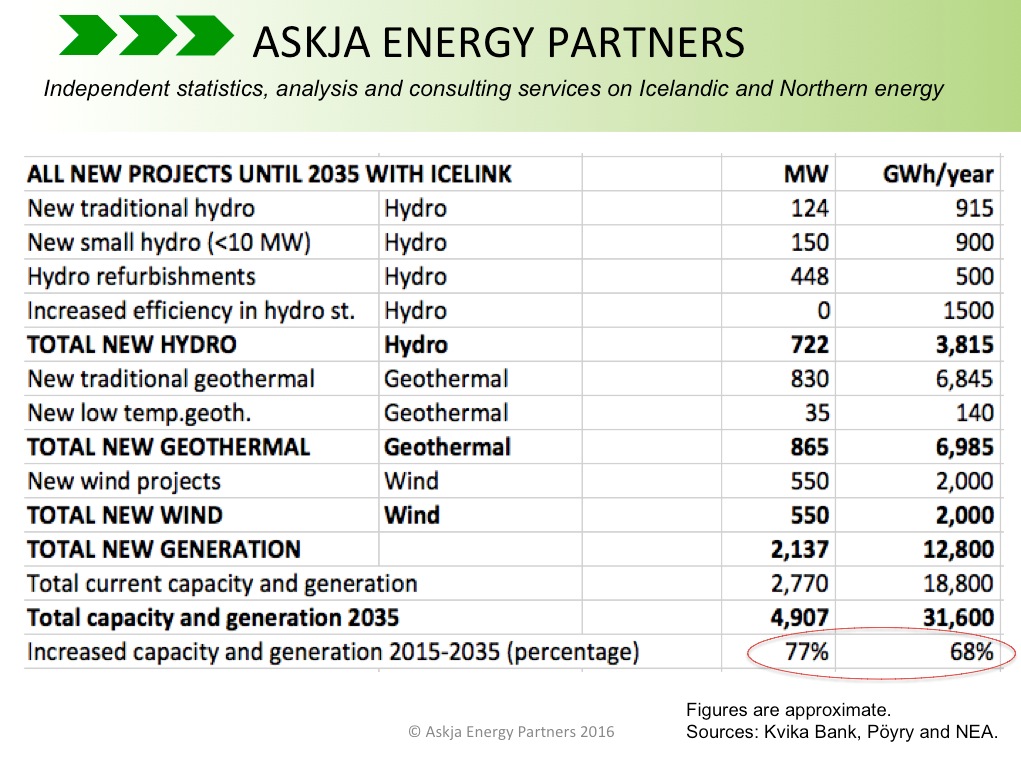

A subsea HVDC power cable between Iceland and the United Kingdom (UK) would call for proportionally extreme increase in Iceland’s generation capacity. According to a new report by Kvika Bank and Pöyry, Iceland needs to build new power capacity of 2,137 MW to supply both the cable and the domestic demand. The figure for the necessary new capacity for the cable only is expected to be 1.459 MW (as shown on the table below). The rest of the new capacity is to meet expected increase in domestic demand for electricity (until 2035).

The cable is normally referred to as IceLink. The report by Kvika and Pöyry (available in Icelandic only) claims that high proportion of the needed new capacity for IceLink can be met with wind power (today Iceland has very small wind power industry, as new geothermal- and hydropower projects have been the least costly way to generate electricity in Iceland). The authors of the report expect that 550 MW of new wind power would be constructed to meet demand by the cable.

The cable is normally referred to as IceLink. The report by Kvika and Pöyry (available in Icelandic only) claims that high proportion of the needed new capacity for IceLink can be met with wind power (today Iceland has very small wind power industry, as new geothermal- and hydropower projects have been the least costly way to generate electricity in Iceland). The authors of the report expect that 550 MW of new wind power would be constructed to meet demand by the cable.

The second largest increase in Icelandic power capacity would be in the form of hydropower refurbishments (which would probably mostly be new turbines in current hydropower stations). This figure is expected to be 448 MW. However, the report does not explain in a clear manner how these refurbishments would be carried out. From the report it is also somewhat unclear why it is believed that 550 MW of new wind power will be a good opportunity for the business case – instead of for example somewhat less wind power and somewhat more hydropower.

Substantial part of the expected new Icelandic capacity until 2035 would come from new small hydropower stations. Such new small hydropower stations, each with a capacity less than 10 MW, would in total be close to 150 MW. This would probably mean dozens of new small running-river hydropower projects in Iceland. Such projects tend to be more costly than the traditional large Icelandic hydropower projects. However, high strike price for the electricity make such expensive projects financially viable, according to the report.

Substantial part of the expected new Icelandic capacity until 2035 would come from new small hydropower stations. Such new small hydropower stations, each with a capacity less than 10 MW, would in total be close to 150 MW. This would probably mean dozens of new small running-river hydropower projects in Iceland. Such projects tend to be more costly than the traditional large Icelandic hydropower projects. However, high strike price for the electricity make such expensive projects financially viable, according to the report.

According to the report, 276 MW of new traditional hydro- and geothermal power will be needed to meet demand from the cable. Most of this capacity will be in geothermal (245 MW).

When also taking increased domestic power demand into account, the total new traditional hydro- and geothermal capacity needed by 2035 is expected to be 954 MW; 124 MW in traditional large hydropower and 830 MW in traditional geothermal power. Today, Iceland has 665 MW of geothermal power (and 1,986 MW of hydropower). So the expected increase in utilization of Icelandic geothermal power is quite enormous. It should be noted that figures on traditional hydro- and geothermal power projects in the report are based on the Icelandic Master Plan for Nature Protection and Energy Utilization.

When also taking increased domestic power demand into account, the total new traditional hydro- and geothermal capacity needed by 2035 is expected to be 954 MW; 124 MW in traditional large hydropower and 830 MW in traditional geothermal power. Today, Iceland has 665 MW of geothermal power (and 1,986 MW of hydropower). So the expected increase in utilization of Icelandic geothermal power is quite enormous. It should be noted that figures on traditional hydro- and geothermal power projects in the report are based on the Icelandic Master Plan for Nature Protection and Energy Utilization.

According to the report, considerable part of the new Icelandic power capacity to be developed is to meet expected increased demand from heavy industries in Iceland. Today, heavy industries in Iceland (which are mostly aluminum smelters) consume close to 80% of all electricity generated in the country. According to the report by Kvika Bank and Pöyry on IceLink, all the three aluminum smelters in Iceland will continue their operations in the coming years and decades. And the authors of the report expect that in the coming years and decades power demand of heavy industries in Iceland will increase. It is noteworthy that such assumptions could change dramatically, if for example one of the aluminum smelters in Iceland would close down.

Finally we should mention that if/when IceLink will be constructed, it is expected that the total increased power capacity in Iceland will be around 77% (increase from beginning of 2016). The increase in generation will be somewhat more or close to 68%. According to the above mentioned report, all the projects to meet this increase will be developed in the next 15-20 years. We will soon be revisiting this subject, explaining in more details what power projects will be needed to meet this high increase. Obviously such an increase will/would make Iceland’s position as the world’s largest electricity producer even more pronounced.

Finally we should mention that if/when IceLink will be constructed, it is expected that the total increased power capacity in Iceland will be around 77% (increase from beginning of 2016). The increase in generation will be somewhat more or close to 68%. According to the above mentioned report, all the projects to meet this increase will be developed in the next 15-20 years. We will soon be revisiting this subject, explaining in more details what power projects will be needed to meet this high increase. Obviously such an increase will/would make Iceland’s position as the world’s largest electricity producer even more pronounced.