New power tariffs to Aluminum smelters

As we explained in a recent article, the Icelandic national power company Landsvirkjun has signed a new contract with the Century Aluminum smelter in Iceland (Norðurál). In this article we will compare the power tariff in this new contract with three other recent power agreements with smelters in Iceland and Canada.

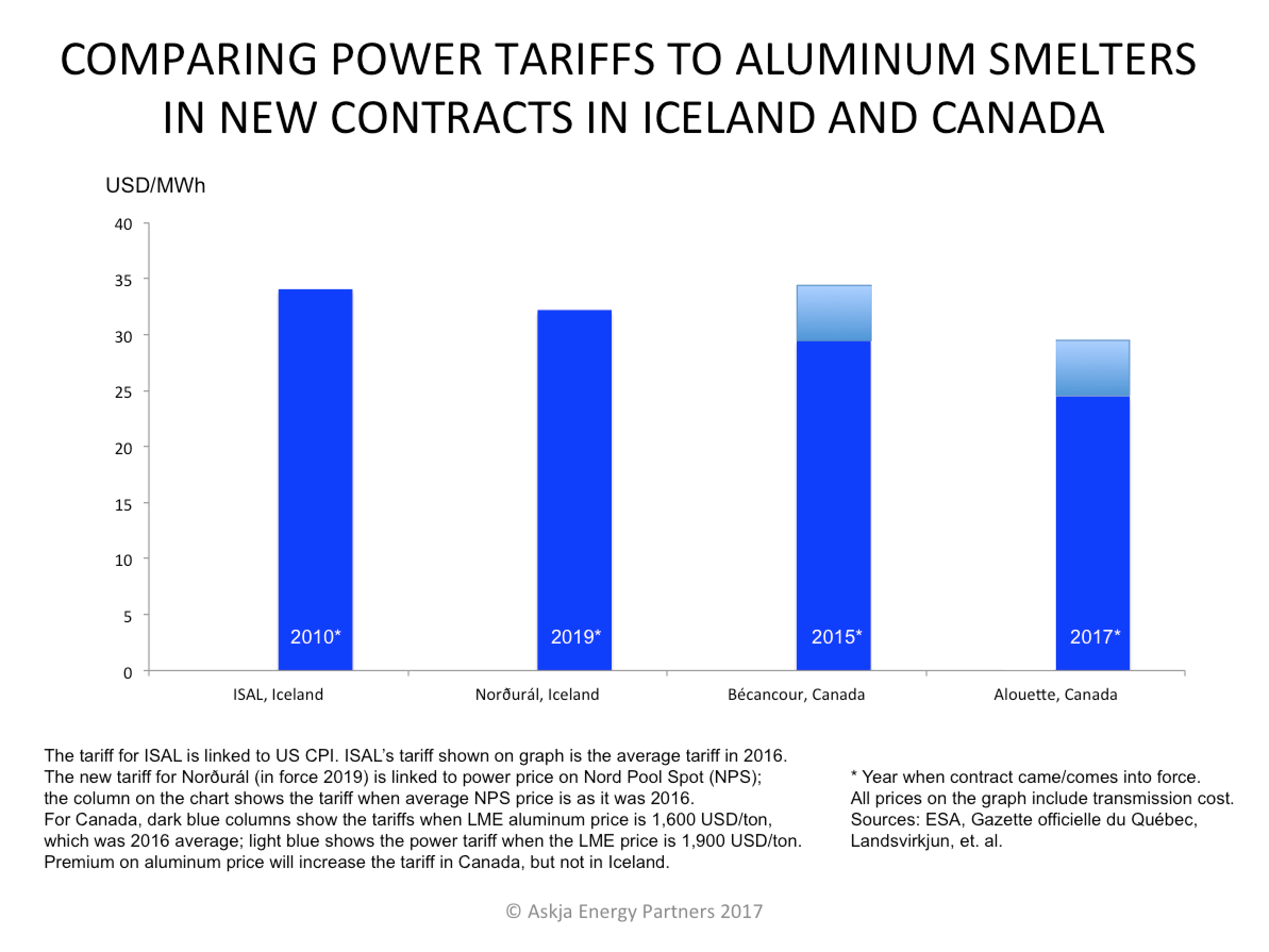

In our comparison we analysed information about four recent power contracts. They are, in addition to the new Norðurál-contract, a contract between Landsvirkjun and ISAL/RTA regarding the smelter at Straumsvík in Southwestern Iceland, a contract between Hydro Québec and Alcoa/RTA regarding the Bécancour smelter in Québec in Canada, and finally a contract between Hydro Québec and Aluminerie Alouette regarding the Sept-Iles smelter, also in Québec. These four contracts were concluded in the period 2010-2016 and they came / will come into force in the period 2010-2019 (as shown on the graph below).

In our comparison we analysed information about four recent power contracts. They are, in addition to the new Norðurál-contract, a contract between Landsvirkjun and ISAL/RTA regarding the smelter at Straumsvík in Southwestern Iceland, a contract between Hydro Québec and Alcoa/RTA regarding the Bécancour smelter in Québec in Canada, and finally a contract between Hydro Québec and Aluminerie Alouette regarding the Sept-Iles smelter, also in Québec. These four contracts were concluded in the period 2010-2016 and they came / will come into force in the period 2010-2019 (as shown on the graph below).

Each of the four contracts are different from the others. Both of the Canadian contracts are long-term and the price of the electricity in both of them is linked to the price-development of aluminum at the London Metal Exchange (LME). However, these two Canadian contracts are based on different prerequisites, as one of them (the Aluminerie Alouette contract) involves an obligation for conducting an engineering study for a potential later expansion of the smelter.

The two Icelandic contracts do not include any price-link with aluminum. The contract with ISAL/RTA from 2010 has a fixed starting tariff, linked to US consumer price index (CPI). The tariff in the more recent contract with Century’s Norðurál is linked to power price at the Nordic power market (Elspot on Nord Pool Spot; NPS).

The contract with ISAL, which was concluded and came into force in 2010, is a long-term contract of 25 years. The contract with Norðurál, agreed in 2016, will come into force in 2019 and only has a duration of four years. The contracting parties, Landsvirkjun and Norðurál, have offered no explanation about why the time-period of the new contract is so short, but an obvious reason is the new tariff being strongly aligned with spot market price of electricity on NPS (as explained in our last post).

The graph at left shows a.o. the approximate average tariff to the Straumsvík smelter of ISAL/RTA in 2016 (the tariff can be expected to rise steadily, as it is linked to the US CPI). The power price paid by Bécancour and Alouette depend on the development of aluminum price, and the blue columns reflect the average base-tariff for these two Canadian smelters in 2016 (when average aluminum price was close to 1,600 USD/ton). The light-blue part of the tariff shows how the Canadian tariff will rise if/when aluminum price becomes 1,900 USD/ton, as recently happened.

The graph at left shows a.o. the approximate average tariff to the Straumsvík smelter of ISAL/RTA in 2016 (the tariff can be expected to rise steadily, as it is linked to the US CPI). The power price paid by Bécancour and Alouette depend on the development of aluminum price, and the blue columns reflect the average base-tariff for these two Canadian smelters in 2016 (when average aluminum price was close to 1,600 USD/ton). The light-blue part of the tariff shows how the Canadian tariff will rise if/when aluminum price becomes 1,900 USD/ton, as recently happened.

We should add that when there is a premium paid for aluminum, as has been the norm most of the time in recent years, the Canadian tariffs will increase, according to a certain formula in the two contracts. Note that the Canadian tariffs shown on the graph are as when the premium is zero. If/when there will be a premium, the power tariffs to the said Canadian smelters will be somewhat higher.

Due to limited information, it is still not possible to claim with precision what is the new base-tariff for the Norðurál smelter at Grundartangi in Iceland (which goes into force in 2019). We do, however, know that the new tariff will be linked or aligned to the electricity price on NPS. EFTA Surveillance Authority (ESA) has stated that “Norðurál’s payments to Landsvirkjun for the electricity each month will be tied to the market price for power in the Nordpool Elspot power market (Elspot System Price reference used)“. ESA also says that “pricing mechanism and the risk associated with using the Nordpool Elspot power prices is […] in line with standard commercial practices of competing power companies in the Nordic countries”, and that the “alignment […] with the Nordpool power prices, allows Landsvirkjun to sell power at the same prices as competing companies in the Nordic countries.”

With regard to the above mentioned statements by ESA, we can assume that the new tariff to the Norðurál smelter will be similar or even the same as the tariff paid by industries in the Nordic market. Furthermore, the statements by ESA strongly imply that the new base-tariff to Norðurál is actually the same as the spot price for electricity on NPS (or at least very close to the spot price). Thus, the new tariff to Norðurál shown on the graph above is the same as the average spot price on NPS in 2016 (Elspot) – with certain part of the transmission cost added (the part of the transmission cost which is not included in the Elspot-price).

With regard to the above mentioned statements by ESA, we can assume that the new tariff to the Norðurál smelter will be similar or even the same as the tariff paid by industries in the Nordic market. Furthermore, the statements by ESA strongly imply that the new base-tariff to Norðurál is actually the same as the spot price for electricity on NPS (or at least very close to the spot price). Thus, the new tariff to Norðurál shown on the graph above is the same as the average spot price on NPS in 2016 (Elspot) – with certain part of the transmission cost added (the part of the transmission cost which is not included in the Elspot-price).

Of course it is possible that the new base-tariff for Norðurál from 2019 may be somewhat lower than the full Elspot-price, as power companies on the Nordic power market may sometimes offer its largest customers a discount from the spot-price on NPS. However, when having regard to the statements of ESA, and with regard to Landsvirkjun’s tariffs to ISAL/RTA, it seems unlikely that the new contract will be offering Norðurál large discount from the Elspot-price.

Finally, note that the assumed new tariff to Norðurál shown on the graph(s) includes the transmission cost that the aluminum firm has to pay to the Icelandic TSO; Landsnet. And note also that Norðurál will continue to pay its current very low tariff to Landsvirkjun until 2019 (when the new power contract enters into force).

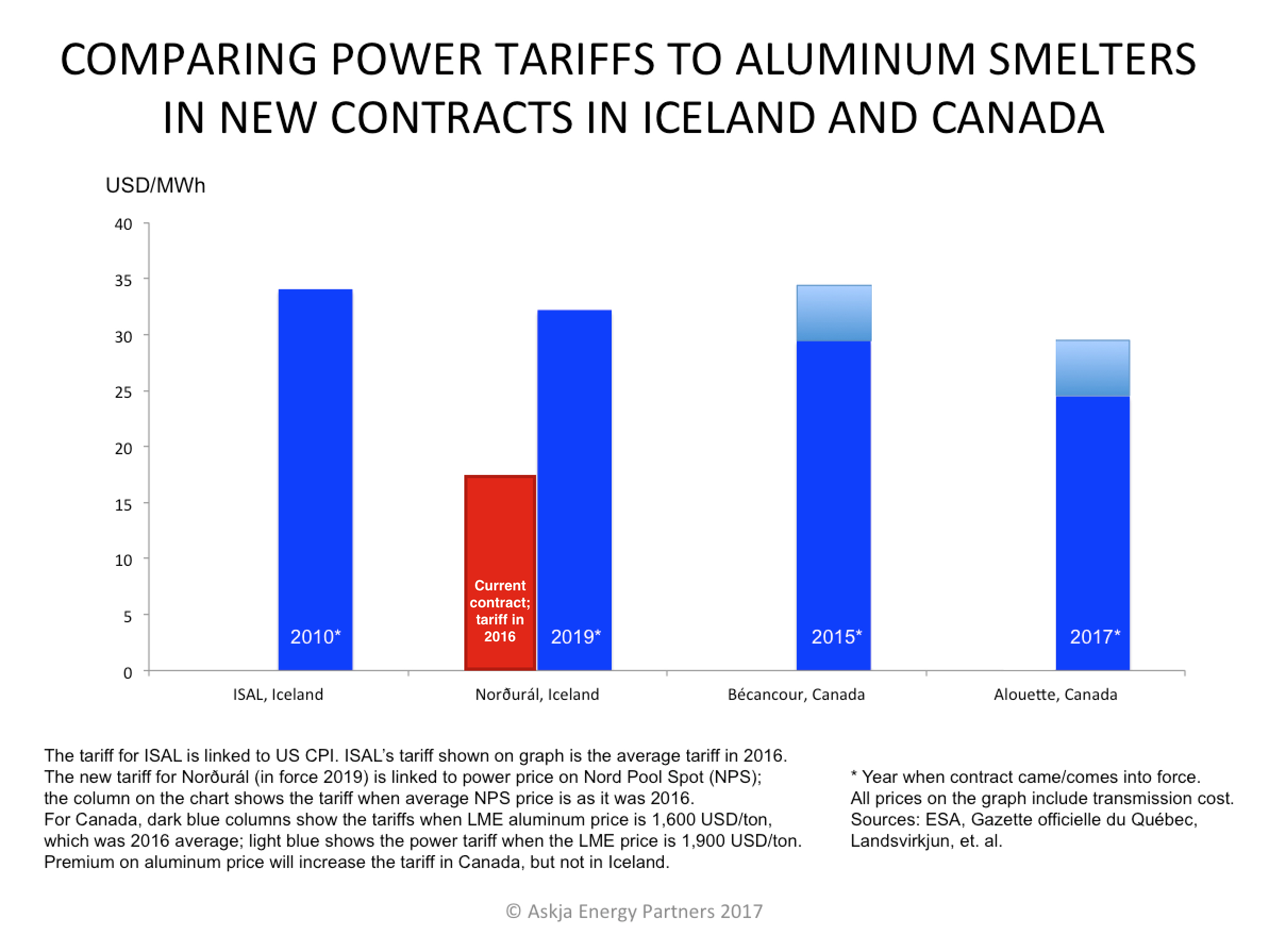

The power tariff Norðurál is currently paying Landsvirkjun happens to be one of the lowest electricity price enjoyed by any of the world’s two hundred-plus aluminum smelters (Norðurál also buys substantial amount of electricity from two other Icelandic power firms, where the average price is only slightly higher than the tariff it pays to Landsvirkjun). Last year (2016), the average price Norðurál paid for the electricity from Landsvirkjun was well below 20 USD/MWh (transmission cost included), as shown on the graph at left (the red column). So it is obvious that the new contract, coming into force in 2019, will increase Landsvirkjun’s revenues substantially – unless we will experience extremely low prices for electricity on the Nordic Elspot power market during 2019-2023.

The power tariff Norðurál is currently paying Landsvirkjun happens to be one of the lowest electricity price enjoyed by any of the world’s two hundred-plus aluminum smelters (Norðurál also buys substantial amount of electricity from two other Icelandic power firms, where the average price is only slightly higher than the tariff it pays to Landsvirkjun). Last year (2016), the average price Norðurál paid for the electricity from Landsvirkjun was well below 20 USD/MWh (transmission cost included), as shown on the graph at left (the red column). So it is obvious that the new contract, coming into force in 2019, will increase Landsvirkjun’s revenues substantially – unless we will experience extremely low prices for electricity on the Nordic Elspot power market during 2019-2023.